Sri Lanka's debt situation; what are our options?

by Dinesh Weerakkody

The external financing situation for Sri Lanka is certainly a big

worry for the government and the private sector. This is largely due to

the monstrous financial profligacy of the past not yet fully explained

and also due to a large trade deficit and a drop in exports and worker

remittances.

In 2015, the Sri Lanka trade deficit was around $ 8.5 billion. Worker

remittances were around $ 6.9 billion. Capital flows were negative. We

had a Balance of Payment deficit of $ 1.5 billion. In 2015, the Sri Lanka trade deficit was around $ 8.5 billion. Worker

remittances were around $ 6.9 billion. Capital flows were negative. We

had a Balance of Payment deficit of $ 1.5 billion.

The only upside in 2015, was tourism with $ 3 billion - a 24%

increase. If the trade deficit can be managed to around $7 billion, the

higher income from tourism, exports and technology services could help

our Balance of Payments to have a surplus.

Other challenges

However, there are many other challenges for our external finances

such as the stability of the rupee, declining reserves and capital

flows. Our export income is only around 55% of imports.

Therefore, it is a must that Sri Lanka in the short-term limits

foreign debt financing only for projects that have multiple benefits for

the economy. Furthermore, we need to focus more on debt refinancing,

debt swaps, work hard to attract more FDIs by introducing

investment-friendly policies and re-structure the Board of Investment (BOI)

to support that drive and more importantly manage the export trade

supply side of the equation.

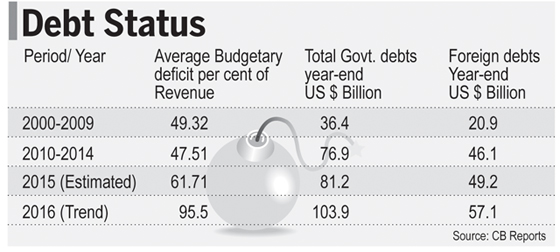

Government debt

Sri Lanka's total government debt at the end of 2015 was US $ 81

billion of which foreign debt was around 60%. According to Central Bank

data, Sri Lanka's total debt will touch US $ 103 billion this year,

around 98% of revenue and foreign debt will increase to US $ 57 billion

this year.

Today, public debt is almost 100% of GDP. Therefore, there is much

work that needs to be done given that we have a BOP deficit of $ 1.5

billion from 2015 to manage first.

Many of the short-term loans taken at exorbitant rates taken for

unproductive projects is one of the root causes for this situation. For

e.g. the Mattala Airport debt arrangement needs to be renegotiated and

those assets need to be productively used for the betterment of society. Many of the short-term loans taken at exorbitant rates taken for

unproductive projects is one of the root causes for this situation. For

e.g. the Mattala Airport debt arrangement needs to be renegotiated and

those assets need to be productively used for the betterment of society.

The IMF Structural Adjustment Facility, if effectively negotiated

could help the economy to ride over this crisis. However, the policy

direction to improve the supply side is a must and tightening of fiscal

and monetary policies.

Way forward for Sri Lanka

While the government is looking for short-term options to ride over

the crisis, such as the recent currency swap with India for US $

1.1billion and the proposed swap with China for US $ 1 billion.

All these arrangements have its cost and political consequences. It

is important from now on to only invest in on-going projects if there

are clear benefits over cost and projects that don't drain our foreign

exchange reserves.

Some of the big-ticket projects such as the Megapolis; mega road

development projects may need to be phased over the next few years.

However, if we are to attract more FDIs, we need to invest more on

education and skills to improve the productivity of the workforce and

improve our inward remittances, given that the dependency of inward

remittances may no longer be sustainable in the long term.

FDI instead of debt financing and foreign borrowings is what we need,

That, however, would need a conducive investment climate that protects

equity-rights, and property rights and deregulation. Sri Lanka urgently

needs a medium-term plan to increase commercial exports and services.

The economy has faced much bigger challenges before. Therefore, given

its strategic location within South Asia and the goodwill we have earned

in the past 12 months with the international community, Sri Lanka should

exploit those opportunities to improve the people's living standards.

The writer is a senior company director. |