Lanka on track to reduce debt levels

In recent times, much has been said about the debt levels of our

country. Some Opposition politicians as well as economists whose

leanings towards the Opposition are well-known, have been ringing alarm

bells that the country is fast moving into a debt trap. In recent times, much has been said about the debt levels of our

country. Some Opposition politicians as well as economists whose

leanings towards the Opposition are well-known, have been ringing alarm

bells that the country is fast moving into a debt trap.

Others including the Central Bank and the Ministry of Finance have

countered that the debt levels are sustainable. This matter is obviously

a critical one, since the Eurozone debt crisis has shown what could

happen if the debt levels of a country get out of hand.

In that background, it would be appropriate to examine the country's

debt issue in a dispassionate, non-political and professional manner, so

as to assess whether the risks associated with a country's borrowings

are being addressed by the relevant authorities in Sri Lanka.

In practice, a person's debt level would be a factor of his income.

This is observed in real life, when a person with a lower income is only

able to borrow a small loan, while a person with a higher income and

assets will be able to obtain bigger advances. Another practical truth

is that if a loan is used for a productive purpose which yields an

income, the viability of such a loan is generally greater, than if the

loan is used for mere consumption.

The repayment capability of a loan is better, if the repayment is

over a longer period of time. In addition, the interest rate is usually

higher, if the credit worthiness of the borrower is low which leads the

lender to demand a higher interest rate to compensate his risk, or in

times of higher inflation in the country.

The above practical considerations that are applicable to any

borrower, also apply in a more sophisticated and complex manner to

countries and governments as well. Therefore, a pragmatic and practical

reasoning must be applied in a sensible manner, when assessing the

sustainability of the debt of a country. The above practical considerations that are applicable to any

borrower, also apply in a more sophisticated and complex manner to

countries and governments as well. Therefore, a pragmatic and practical

reasoning must be applied in a sensible manner, when assessing the

sustainability of the debt of a country.

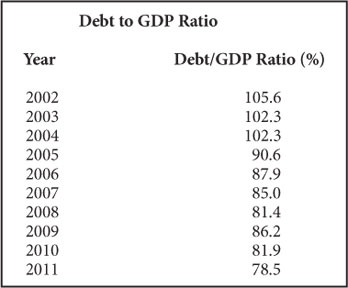

In the case of a country, the capacity for repayment is primarily

evaluated through the Debt to GDP ratio. Sri Lanka's Debt to GDP ratio

over the past 10 years is shown in the table.

It indicates that Sri Lanka is on a clear path of reducing its debt

levels in comparison to its GDP. That is a step in the right direction.

At the same time, there have been reports issued by the Central Bank

that they are attempting to reduce the debt to GDP level to about 60

percent by 2016.

That attempt too, would be useful since it would lead the country to

a comfortable debt level, which would be a significant improvement from

the alarming level of over 105 percent ten years ago.

Over the past six years, the Central Bank has stated that new loans

have been obtained to fund viable infrastructure development projects

only. If such a discipline is exerted over the debt dynamics, the

overall sustainability of the Debt would certainly be enhanced. In the

period prior to 2001, massive loans of over US$ 600 million had been

obtained for the import and consumption of wheat flour.

Needless to say, those consumption-based foreign currency loans have

imposed a major burden on the economy since no economic activities and

resultant revenue has been earned from the corresponding application of

the borrowed foreign funds. Therefore, the Government's firm commitment

that it will not obtain loans of such nature is certainly welcome.

In the meantime, the Central Bank has stated that it is implementing

a strategy of consciously extending the overall repayment period of its

portfolio. Such a strategy too is useful, since an extended repayment

period would apply lower pressure on the debt repayment schedule, which

would, in turn, help improve debt sustainability further.

As is well-known, Sri Lanka has traditionally been a high inflation

nation where inflation has been in double digit numbers for long periods

of time. Of late however, Sri Lanka has been able to maintain inflation

at single digit levels, and has done so for the past 42 months. This

achievement has helped to maintain interest rates at reasonable levels.

Nevertheless, the country's interest rates are still higher than in

other developed nations, and this situation needs to be addressed over

the next few years. Maintaining inflation and interest rates at

reasonable levels, while improving macro fundamentals in a consistent

manner and thereby upgrading the country's credit rating, will help Sri

Lanka to access funds at lower interest rates in time to come. Nevertheless, the country's interest rates are still higher than in

other developed nations, and this situation needs to be addressed over

the next few years. Maintaining inflation and interest rates at

reasonable levels, while improving macro fundamentals in a consistent

manner and thereby upgrading the country's credit rating, will help Sri

Lanka to access funds at lower interest rates in time to come.

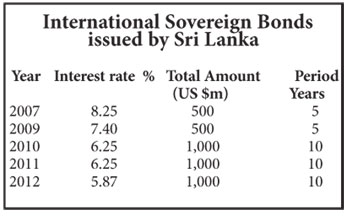

Fortunately, there seems to be a macro level plan and effort to

achieve such an outcome, and that is encouraging. The interest rates

secured by the country in its past international bond issues also seem

to suggest a growing credit worthiness of Sri Lanka as viewed by its

expanding network of international investors .

The above analysis should provide some comfort to an unbiased

stakeholder that Sri Lanka is on a sustainable debt path, unlike some

advanced countries that are struggling with heavy debt burdens.

Therefore, there should no cause for unnecessary apprehension and panic,

as predicted by some politicians and economists.

However, it is necessary for the Government and the Central Bank to

keep in mind that the current global debt dynamics is highly complex and

volatile, and therefore the on-going commitment to reduce the Government

fiscal deficit and deliver benign levels of inflation must be continued

in earnest. That approach would certainly provide a lot of confidence to

all stakeholders of the economy.

|

")