Global economic prospects to improve this year - World Bank

Following another disappointing year in 2014, developing countries

should see an uptick in growth this year, boosted in part by soft oil

prices, a stronger U.S. economy, continued low global interest rates,

and receding domestic headwinds in several large emerging markets, says

the World Bank Group's 'Global Economic Prospects' (GEP) report,

released today.

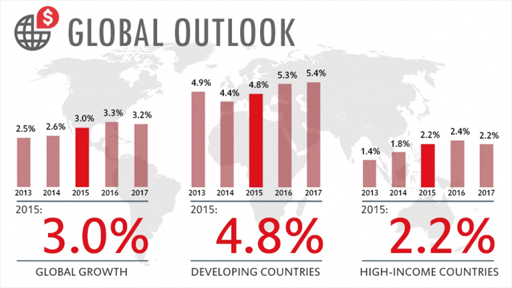

After growing by an estimated 2.6 percent in 2014, the global economy

is projected to expand by 3 percent this year, 3.3 percent in 2016 and

3.2 percent in 2017, predicts the Bank's twice-yearly flagship report.

Developing countries grew by 4.4 percent in 2014 and are expected to

edge up to 4.8 percent in 2015, strengthening to 5.3 and 5.4 percent in

2016 and 2017. Developing countries grew by 4.4 percent in 2014 and are expected to

edge up to 4.8 percent in 2015, strengthening to 5.3 and 5.4 percent in

2016 and 2017.

"In this uncertain economic environment, developing countries need to

judiciously deploy their resources to support social programs with a

laser-like focus on the poor and undertake structural reforms that

invest in people," said World Bank Group President Jim Yong Kim.

"It's also critical for countries to remove any unnecessary

roadblocks for private sector investment. The private sector is by far

the greatest source of jobs and that can lift hundreds of millions of

people out of poverty."

Underneath the fragile global recovery lie increasingly divergent

trends with significant implications for global growth. Activity in the

United States and the United Kingdom is gathering momentum as labour

markets heal and monetary policy remains extremely accommodative.

But the recovery has been sputtering in the Euro Area and Japan as

legacies of the financial crisis linger. China, meanwhile, is undergoing

a carefully managed slowdown with growth slowing to a still-robust 7.1

percent this year (7.4 percent in 2014), 7 percent in 2016 and 6.9

percent in 2017.

And the oil price collapse will result in winners and losers. Risks

to the outlook remain tilted to the downside, due to four factors. First

is persistently weak global trade. Second is the possibility of

financial market volatility as interest rates in major economies rise on

varying timelines.

Third is the extent to which low oil prices strain balance sheets in

oil-producing countries. Fourth is the risk of a prolonged period of

stagnation or deflation in the Euro Area or Japan.

"Worryingly, the stalled recovery in some high-income economies and

even some middle-income countries may be a symptom of deeper structural

malaise," said World Bank Chief Economist and Senior Vice President,

Kaushik Basu.

"As population growth has slowed in many countries, the pool of

younger workers is smaller, putting strains on productivity. But there

are some silver linings behind the clouds. The lower oil price, which is

expected to persist through 2015, is lowering inflation worldwide and is

likely to delay interest rate hikes in rich countries.

"This creates a window of opportunity for oil-importing countries,

such as China and India, we expect India's growth to rise to 7 percent

by 2016. What is critical is for nations to use this window to usher in

fiscal and structural reforms, which can boost long-run growth and

inclusive development."

On the back of gradually recovering labour markets, less budget

tightening, soft commodity prices, and still-low financing costs, growth

in high-income countries as a group is expected to rise modestly to 2.2

percent this year (from 1.8 percent in 2014) in 2015 and by about 2.3

percent in 2016-17.

Growth in the United States is expected to accelerate to 3.2 percent

this year (from 2.4 percent last year), before moderating to 3 and 2.4

percent in 2016 and 2017, respectively. In the Euro Area, uncomfortably

low inflation could prove to be protracted.

The forecast for Euro Area growth is a sluggish 1.1 percent in 2015

(0.8 percent in 2014), rising to 1.6 percent in 2016-17. In Japan,

growth will rise to 1.2 percent in 2015 (0.2 percent in 2014) and 1.6

percent in 2016. Trade flows are likely to remain weak in 2015. Since

the global financial crisis, global trade has slowed significantly,

growing by less than 4 percent in 2013 and 2014, well below the

pre-crisis average growth of 7 percent per annum.

The slowdown is partly due to weak demand and to what appears to be

lower sensitivity of world trade to changes in global activity, finds

analysis in the report. Changes in global value chains and a shifting

composition of import demand may have contributed to the decline in

responsiveness of trade to growth.

Commodity prices are projected to stay soft in 2015. As discussed in

a chapter in the report, the unusually steep decline in oil prices in

the second half of 2014 could significantly reduce inflationary

pressures and improve current account and fiscal balances in

oil-importing developing countries.

"Lower oil prices will lead to sizeable real income shifts from

oil-exporting to oil-importing developing countries. For both exporters

and importers, low oil prices present an opportunity to undertake

reforms that can increase fiscal resources and help broader

environmental objectives,"

said Director of Development Prospects at the World Bank, Ayhan Kose.

Among large middle-income countries that will benefit from lower oil

prices is India, where growth is expected to accelerate to 6.4 percent

this year (from 5.6 percent in 2014), rising to 7 percent in 2016-17.

In Brazil, Indonesia, South Africa and Turkey, the fall in oil prices

will help lower inflation and reduce current account deficits, a major

source of vulnerability for many of these countries. However, sustained

low oil prices will weaken activity in exporting countries.

For example, the Russian economy is projected to contract by 2.9

percent in 2015, getting barely back into positive territory in 2016

with growth expected at 0.1 percent.

In contrast to middle-income countries, economic activity in

low-income countries strengthened in 2014 on the back of rising public

investment, significant expansion of service sectors, solid harvests,

and substantial capital inflows.

Growth in low-income countries is expected to remain strong at 6

percent in 2015-17, although the moderation in oil and other commodity

prices will hold growth back in commodity exporting low-income

countries.

"Risks to the global economy are considerable. Countries with

relatively more credible policy frameworks and reform-oriented

governments will be in a better position to navigate the challenges of

2015," concluded Franziska Ohnsorge, lead author of the report.

Regional highlights

The East Asia and Pacific region continued its gradual adjustment to

slower but more balanced growth. Regional growth slipped to 6.9 percent

in 2014 as a result of policy tightening and political tensions that

offset a rise in exports in line with the ongoing recovery in some

high-income economies.

The medium-term outlook is for a further easing of growth to 6.7

percent in 2015 and a stable outlook thereafter, reflecting a gradual

slowdown in China, which will be offset by a pick-up in the rest of the

region in 2016-17.

In China, structural reforms, a gradual withdrawal of fiscal

stimulus, and continued prudential measures to slow non-bank credit

expansion will result in slowing growth to 6.9 percent by 2017 (from 7.4

percent in 2014).

In the rest of the region, excluding China, growth will strengthen to

5.5 percent by 2017 (from 4.6 percent in 2014) supported by firming

exports, improved political stability, and strengthening investment.

Growth in developing Europe and Central Asia is estimated to have

slowed to a lower-than-expected 2.4 percent in 2014 as a sputtering

recovery in the Euro Area and stagnation in Russia posed headwinds.

In contrast, growth in Turkey exceeded expectations despite slowing

to 3.1 percent. Regional growth is expected to rebound to 3 percent in

2015, 3.6 percent in 2016 and 4 percent in 2017 but with considerable

divergence.

Recession in Russia holds back growth in Commonwealth of Independent

States whereas a gradual recovery in the Euro Area should lift growth in

Central and Eastern Europe and Turkey.

The tensions between Russia and Ukraine and the associated economic

sanctions, the possibility of prolonged stagnation in the Euro area, and

sustained commodity price declines remain key downside risks for the

region.

Growth in Latin America and the Caribbean slowed markedly to 0.8

percent in 2014, but with diverging developments across the region.

South America slowed sharply as domestic factors, exacerbated by

economic slowdown in major trading partners and declining global

commodity prices, took their toll on some of the largest economies in

the region.

In contrast, growth in North and Central America was robust, lifted

by strengthening activity in the United States. Strengthening exports on

the back of the continued recovery among high-income countries and

robust capital flows should lift regional GDP growth to an average of

around 2.6 percent in 2015-17.

A sharper-than-expected slowdown in China and a steeper decline in

commodity prices represent major downward risks to the outlook.

Following years of turmoil, some economies in the Middle East and

North Africa appear to be stabilising, although growth remains fragile

and uneven. Growth in oil-importing countries was broadly flat in 2014,

while activity in oil-exporting countries recovered slightly after

contracting in

2013. Fiscal and external imbalances remain significant.

Regional growth is expected to pick up gradually to 3.5 percent in

2017 (from 1.2 percent in 2014). Risks from regional turmoil and from

the volatile price of oil are considerable; political transitions and

security challenges persist.

Measures to address long-standing structural challenges have been

repeatedly delayed and high unemployment remains a key challenge. Lower

oil prices offer an opportunity to remove the region's heavy energy

subsidies in oil-importing countries.

In South Asia, growth rose to an estimated 5.5 percent in 2014 from a

10-year low of 4.9 percent in 2013. The upturn was driven by India, the

region's largest economy, which emerged from two years of modest growth.

Regional growth is projected to rise to 6.8 percent by 2017, as

reforms ease supply constraints in India, political tensions subside in

Pakistan, remittances remain robust in Bangladesh and Nepal and demand

for the region's exports firms.

Past adjustments have reduced vulnerability to financial market

volatility. Risks are mainly domestic and of a political nature.

Sustaining the pace of reform and maintaining political stability are

key to maintaining the recent growth momentum.

In Sub-Saharan Africa, growth picked up only moderately in 2014 to

4.5 percent, reflecting a slowdown in several of the region's large

economies, notably South Africa.

Growth is expected to remain flat in 2015 at 4.6 percent (lower than

previously expected), largely due to softer commodity prices, and rise

gradually to 5.1 percent by 2017, supported by infrastructure

investment, increased agriculture production, and buoyant services.

The outlook is subject to significant downside risks arising from a

renewed spread of the Ebola epidemic, violent insurgencies, lower

commodity prices, and volatile global financial conditions.

Policy priorities include a need for budget restraint for some

countries in the region and a shift of spending to increasingly

productive ends, as infrastructure constraints are acute. Project

selection and management could be improved with greater transparency and

accountability in the use of public resources. |

")